October 2022 Consumer Sentiment Index | Published: 20/10/2022

Budget boost helps deliver small uptick in Irish consumer sentiment in October

-

Budget ’23 support measures produce a limited easing in financial concerns ….

-

….but sentiment index still at depressed levels suggesting Irish consumers remain gloomy

-

Impact of recent UK difficulties unclear but some hints that Irish consumers encouraged by comparatively stable and supportive domestic policy settings and stability

-

October results point to very cautious consumer spending in run-up to Christmas

The Credit Union Consumer Sentiment Index improved slightly in October as a range of measures announced in Budget ’23 offered a partial offset to the economic uncertainty and financial pressures that have caused Irish consumer confidence to tumble through 2022.

Despite the small uplift in October, it remains the case that Irish consumer sentiment is very weak at present. Only 10 of the previous 320 readings in the near twenty-seven-year history of the survey were weaker than the current figure. As such, the Credit Union Consumer Sentiment Index implies Irish consumers are very gloomy about the circumstances they now face.

The consumer sentiment index is focussed exclusively on economic and financial factors affecting Irish households. However, it would be surprising if the awful tragedy that unfolded in Creeslough Donegal during the survey period did not weigh in some manner on the thinking of consumers, darkening the assessment of current circumstances.

While Irish consumers may be gloomy, the small improvement in confidence in October hints that they still have the capacity to see some silver lining in a generally dark economic sky. In a survey period that saw notable downgrades to a range of economic forecasts at home and abroad, and repeated signals from the European Central Bank that further large interest rate increases are planned for coming months, our judgement is that this pick-up primarily reflects a response to Budget’23 support measures.

At the margin, it may also be that Irish consumers are drawing some comfort from the view that, in sharp contrast to recent developments in the UK, current domestic policy settings should provide some measure of relief from painful cost of living pressures.

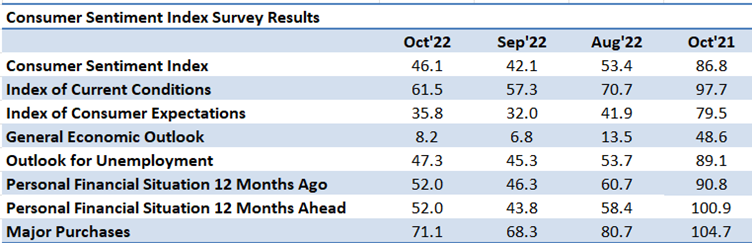

The Credit Union Consumer Sentiment Index increased to 46.1 in October from the 14 year low of 42.1 recorded in September. The 4-point rise in the index this month represents only a limited reversal of the 11.3-point decline seen last month. This likely reflects the fact that the pressures weighing on Irish consumer confidence remain formidable and seem set to intensify as winter weather emphasises how expensive energy costs have become.

The increase in Irish consumer sentiment in October mirrored a further if slightly smaller rise in US consumer sentiment that was sufficient to bring the US measure to a six-month high. We previously noted that falling gasoline prices in the ‘States and notably more modest pressures on light and heating costs than on this side of the Atlantic had provided some element of support to US consumer confidence. A relatively resilient economy centred on a solid jobs market also helped.

It could be that recent falls in Irish petrol prices alongside Budget ’23 measures supporting household spending power helped Irish consumer sentiment in October. So too, could a slight easing in Irish inflation in circumstances where many consumers were braced for ever-accelerating price pressures. At the margin, a still healthy Irish economy, even if it is expected to weaken in the months ahead could also have encouraged a slightly less negative view of the ‘macro’ outlook facing Irish consumers.

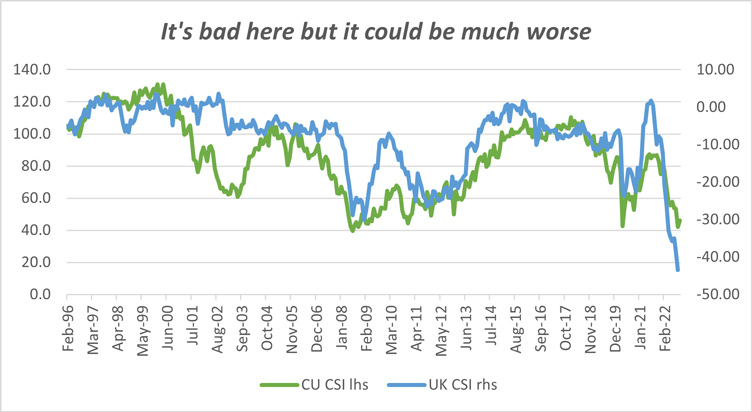

The impact of recent developments in the UK on Irish consumer sentiment is not completely clearcut. To the extent that British economic policy problems weaken the UK economy, this would weigh on the Irish economic outlook but there is not the same mechanically damaging spill-over that caused Irish consumer sentiment to slump during the Brexit process.

On the other hand, it could be argued that high profile UK policy difficulties may encourage Irish consumers to draw some comfort from a notably more stable, sustainable, and supportive domestic economic policy stance in this country.

On balance, we think the contrast between the broad measure of support seen for Budget ’23 measures and the heightened divisions within UK policymaking may have had some small positive influence on the Irish consumer sentiment reading for October. This judgement appears to be supported by the evidence of the diagram below that compares readings from the Credit Union Consumer Sentiment Index for Ireland and a composite measure of UK consumer confidence (derived from the Federal Reserve Economic Database).

Given the predominantly gloomy tone of economic commentary, both domestic and global, through the survey period, it is encouraging that the October survey saw small improvements in both ‘macro’ elements. This likely owes something to three or possibly four factors.

First of all, most of the main Irish economic indicators continue to point towards the persistence of solid growth. Second, the thrust of the measures in Budget ’23 will provide material support is to purchasing power in the months ahead. Finally, at current levels, the sentiment survey suggests Irish consumers are expecting a marked worsening of economic conditions. So, the current reading already discounts a lot of bad news about the economic outlook. Finally, we think the relative stability of domestic policy settings seen in the context of recent UK problems may also have helped the October reading.

The improvement in the Credit Union Consumer Sentiment Index was more pronounced in those elements of the survey focussed on household finances. This might suggest a broadly positive judgement, albeit modestly so, on the measures announced in Budget ’23. The fact that the element of the survey showing most improvement between September and October relates to the prospects for household finances in the next twelve months is encouraging in this regard.

That said, it remains the case that Irish consumers are almost evenly split between those who see their household finances worsening in the next twelve months and those who see them holding steady. Negligible numbers of those surveyed expect any improvement in their finances in the year ahead.

Not surprisingly, this means that despite a slight improvement in spending plans, the buying climate remains overwhelmingly negative. This suggests household spending will continue to be constrained in the run-up to Christmas, but the October survey also hints at some element of resilience that should support confidence and consumer spending in coming months.

The Irish Consumer Sentiment Survey is a monthly survey of a nationally representative sample of 1,000 adults. Since May 2019, Core Research have undertaken the survey administration and data collection for the Survey. The survey was live between the 4th – 13th October 2022.