Consumer sentiment slightly stronger as Christmas spending plans remain cautious.

Posted on: 20 Nov 2023

-

Irish consumer confidence improves again as pressures ease but problems persist

-

Improved mood of Irish consumers in November contrasts with increased gloom in US

-

Reduced ‘macro’ worries may reflect easing inflation and hope that interest rates have peaked

-

Views on household finances mixed as seasonal spending demands increase

- Special question focusses on Christmas spending power and plans

- 1 in 2 consumers have less to spend on Christmas while just 1 in 14 consumers have more to spend than a year ago…

- ….but cutbacks less widespread than a year ago….

- ….as ‘cutback Christmas’ has become the norm in recent years.

- So, a ‘prudent’ Christmas spend being planned..

- and improving sentiment could see some seasonal ‘overshoot’ in spending plans

- Those aged under 35 able and planning to spend more than a year ago

- Those reporting difficulties making ends meet nearly three times more likely to have less Christmas spending power than a year ago

- We present a crude estimate that suggests Christmas costs are likely to be just over 4% higher than a year ago compared to a 6% rise for Christmas ’22.

- Rapidly increasing cost of food and going out partly offset by falling prices for many gifts

Speaking on the release of November data and analysis, David Malone, CEO of the ILCU noted; "The special question in the November Credit Union Consumer Sentiment Survey suggests that Christmas remains a challenging time financially and emphasises the importance of the support network provided by credit unions".

Summary

Irish consumer sentiment edged slightly higher for a second month in November. This mainly reflected a modest easing in concerns about the economic outlook. Falling energy prices and growing hopes that interest rates may have peaked likely prompted this improvement. Coupled with Budget ’24 support measures, these developments also suggest strains on household finances may be less pressing this Christmas than consumers might have feared.

As buying plans remain subdued, the general tone of the sentiment survey for November and responses to the special question asked this month hint at a Christmas of managed caution rather than major cutbacks in household spending.

It may be that small improvements in confidence in each of the past two months at least tentatively point towards the possibility of a more positive trend in Irish consumer sentiment and spending into early 2024.

Section I; Irish consumers see some reasons to be less fearful

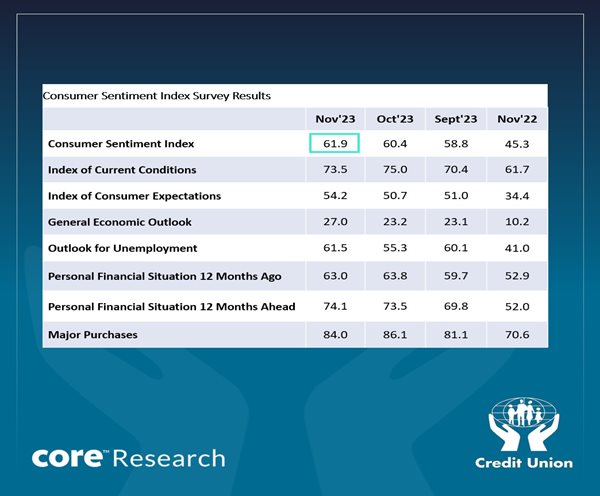

As the table below indicates, the Credit Union Consumer Sentiment Survey (in partnership with Core Research) for November increased to 61.9 from 60.4 in October. The past two months have seen marginal increases that followed successive declines in August and September. As a result, Irish consumer confidence is still running slightly below the levels seen through the summer and remains notably further below the long-term series average of 84.8.

We interpret current survey readings as signalling that the prevailing mood of Irish consumers is one of continuing caution. That said, we think the gains of the past two months, albeit modest, may be hinting that many Irish consumers think the worst could be over in relation to the concerns that have weighed heavily on the sentiment and spending power of households in Ireland and elsewhere in recent years.

Improvement in Irish sentiment contrasts with US gloom

As was the case last month, the improvement in Irish consumer sentiment in November is at odds with a further material drop in US consumer sentiment as measured by the University of Michigan survey (which has now fallen for four months in a row).

The authors of the US report note that a gloomier economic outlook and interest rate worries had a notable impact on younger and poorer consumers in the ‘States while sentiment improved among wealthier consumers. In contrast, confidence improved appreciably among younger and lower income Irish consumers in November while sentiment was more subdued among higher income consumers.

Improved ‘macro’ thinking may seem surprising

Three of the five main components of the Credit Union Consumer Sentiment Survey (in partnership with Core Research) registered stronger readings in November than in October. In contrast to the improvement in the October survey, the gains this month were more pronounced in the survey’s two ‘macro’ elements which focus on the general economic outlook and job prospects.

It is not immediately obvious why the economic concerns of Irish consumers should have eased in November. The improved ‘macro’ survey result might suggest Irish consumers have not been overly focussed on either the negative preliminary GDP reading for Q3 released during the survey period or weaker corporation tax receipts in recent months. In part, this may be because these developments are seen as somewhat removed from the ‘everyday economy’ of most households.

The November survey also saw a reversal of the weakness in consumer thinking on the outlook for jobs that was a notable feature of an otherwise positive survey in October. Again, a couple of high-profile layoff announcements and a rise in the official unemployment rate might have suggested further weakness in this element of the survey. However, there was a contrasting notable fall in numbers on the live register, suggesting contrasting influences in the jobs market at present.

However, it should be emphasised that despite the improvement in this month’s survey, these results still suggest Irish consumers expect economic growth will slow and the jobs market will soften in the next twelve months.

Our sense is that the increasing possibility that interest rates may have peaked (after the ECB left its policy rates unchanged in late October following ten successive rate hikes) and inflation may be easing likely contributed to some easing in ‘macro’ gloom. A fall in global oil prices in the second half of October and early November notwithstanding recent atrocities in the middle east and hopes a global recession may be avoided could also be factors in a slightly less downbeat assessment of the general economic outlook.

While the improvement in Irish consumer sentiment in October was driven primarily by those elements of the survey focussed on household finances, these elements were more mixed in November.

Consumers have mixed views on their financial circumstances

Views on household finances through the past twelve months weakened marginally, perhaps reflecting the reality that although inflation may have eased household living costs continue to climb. In contrast, consumers were a little more positive in relation to the outlook for household finances over the next twelve months. This could reflect the further easing in energy costs and, in particular, a high-profile round of upcoming price cuts from electricity and gas providers.

After an encouraging rise in October, consumers spending plans fell back somewhat in November. Several factors may be at play here. To a significant extent a pullback in spending plans may simply reflect the pressures a notably increased seasonal outlay on light and heating place on spending power. The scale of difficulties in this regard is evident in recent data showing 275,000 domestic customers in arrears on their electricity bills in the third quarter, up 10% on the previous three months.

Two other less negative influences could also be contributing to the pullback in spending plans in the latest survey reading-it is worth emphasising that financial circumstances and drivers of sentiment vary widely across the spectrum of Irish consumers. One possible explanation of softer spending plans in November is that consumers may be temporarily curbing spending ahead of increased outlays over the Christmas period. Given the timing of the November survey which concluded on the 14th of the month, there may also be some element of consumers delaying spending until ‘Black Friday’ price discounts appear.

Section II. Irish consumer spending plans for Christmas 2023.

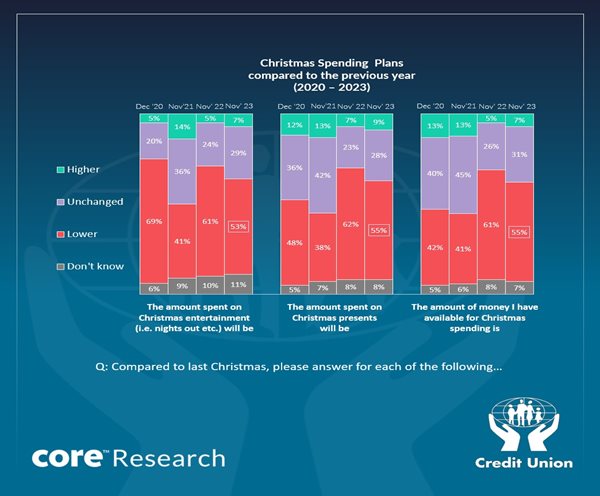

The Credit Union Consumer Sentiment survey (in partnership with Core Research) for November contained a special question focussed on Irish consumers spending plans for Christmas 2023. This also allows a comparison with spending intentions for the previous three years when similar questions were asked.

While Irish inflation is easing, consumers will find that the cumulative and continuing rise in living costs seen through the past two years will markedly reduce discretionary spending power this Christmas.

As the diagram below indicates, just over half of Irish consumers (55%) expect to have less to spend than last Christmas while only 1 in 14 of consumers (7%) say they have more to spend. Indeed, looking at trends over the past four years, it seems that planning to cut back on seasonal spending is now a seasonal norm. This probably reflects a response to a sequence of negative shocks to spending capacity and accessibility over this period.

However, the responses for Christmas ’23 are less negative than last year when the full shock of the cost-of-living crisis was being felt in rapidly accelerating food and energy prices. As a result, slightly more consumers are planning to spend more on presents (9%) than last year (7%) and a similar picture emerges in terms of a planned higher spend on entertainment (7%) against (5%). More significantly, the proportion of consumers intending to cut back on presents (55% against 62%) and on entertainment (53% against 61%) is notably lower than in 2022 although still large in absolute terms.

The impact of higher household bills through the past couple of years means there are significant demographic variations in Christmas spending plans. Those aged under 35 were more notably likely to say they have more to spend this Christmas than those aged over 35. Reflecting this, under 35’s were more than twice as likely to say they will spend more on entertainment this year than older consumers and about twice as likely to say they will spend more on presents.

Not surprisingly, those reporting difficulty making ends were nearly three times more likely to report lower spending power this Christmas, and twice as likely to report lower planned spending as those making ends meet with ease. Conversely those making ends meet with ease were about four times more likely to report greater spending power and increased spending plans than those with financial difficulties.

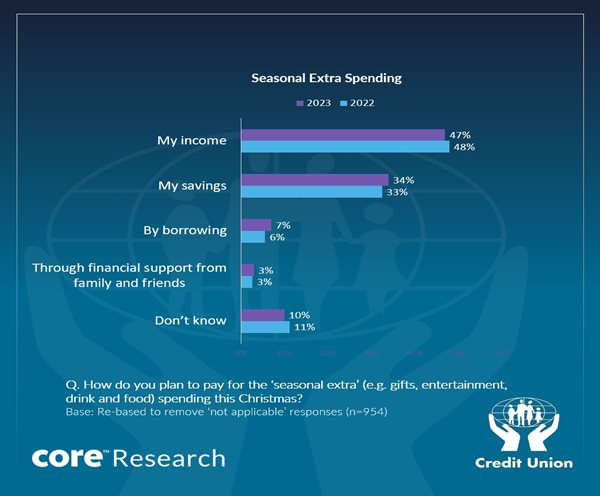

Our sense is that while the general tone of responses to the questions on Christmas spending power and plans is still generally negative, the improvement compared to a year ago hints at resilience and, for some, increased resources. In turn, this might suggest that, compared to last year, a somewhat more positive if ‘prudent’ Christmas spend being planned this year.

With the Credit Union Consumer Sentiment Survey also hinting at some improvement in the mood of Irish consumers at present, continuing good news in relation to energy prices could see the Christmas spending developing more positively than planned. This would imply that households but not all may have the wherewithal to enjoy some element of seasonal cheer next month.

How fast is the cost of Christmas rising?

To give further context to the questions on Christmas spending, we thought it might be useful to get some sense as to how quickly the cost of Christmas-specific spending might be rising in Ireland. The table below presents a fairly crude breakdown of Christmas spending costs for major types of outlay most associated with Christmas spending using a fairly arbitrary weighting of such spending. We then compare the inflation rate for those items using consumer price data for October 2023 (the latest month available) and previous years from the Central Statistics Office.

This admittedly rough exercise suggests the cost of Christmas is rising by a little over 4% this year, a marginally slower pace than the 6% rate seen a year ago but markedly higher than the 0.5% rate seen in 2021. Large and ongoing increases in the cost of food and ‘going out’ are partly offset by falling prices for many gift items.

We should mention that the CSO price data likely imply an underestimate of the cost of the most in-demand toys and probably also understate changes in more expensive jewellery prices. Even ignoring such caveats, these estimates suggest that Irish consumers continue to see a ‘seasonal’ cost-of-living uplift at a time when discretionary spending power is already under significant pressure for many households.

The Credit Union Consumer Sentiment Survey is a monthly survey of a nationally representative sample of 1,000 adults. Since May 2019, Core Research have undertaken the survey administration and data collection for the survey. The November 2023 survey was live between the 2nd and 14th November 2023.