January 2023 Consumer Sentiment Index | Published: 26/01/23

Irish consumer sentiment starts 2023 on a stronger note

-

January sentiment reading at a 7 month high, signalling nervous but not entirely negative Irish consumer

-

Biggest improvement in household finances elements of survey as fuel prices fall, fiscal supports kick in and many households weather Christmas spending better than feared

-

Special 5-year outlook questions suggest marked downgrade to longer-term economic outlook

-

5-year view of household finances notably weaker than twelve months ago with views on house price outlook also more mixed

-

Initial survey of Northern Ireland consumers shows more widespread negativity about economic outlook, but views on household finances not markedly different on either side of the border

Section I; Irish consumers notably less negative at the start of 2023

Irish consumer sentiment rose strongly in January as a softening in oil prices, strong domestic economic data and a seasonal switch-off from business and political news encouraged a less negative if still nervous, view of the economic and financial circumstances of Irish households.

The improvement in Irish consumer sentiment in January mirrored gains in similar confidence measures in the US that likely reflected falling fuel costs and Germany where fiscal supports may also have played a role. In contrast, UK consumer confidence weakened in January reflecting growing negativity about the economy and concerns about the health of the public finances.

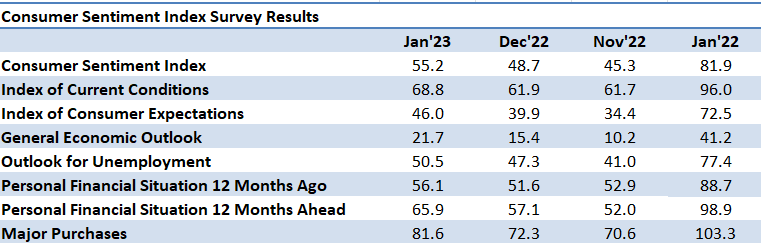

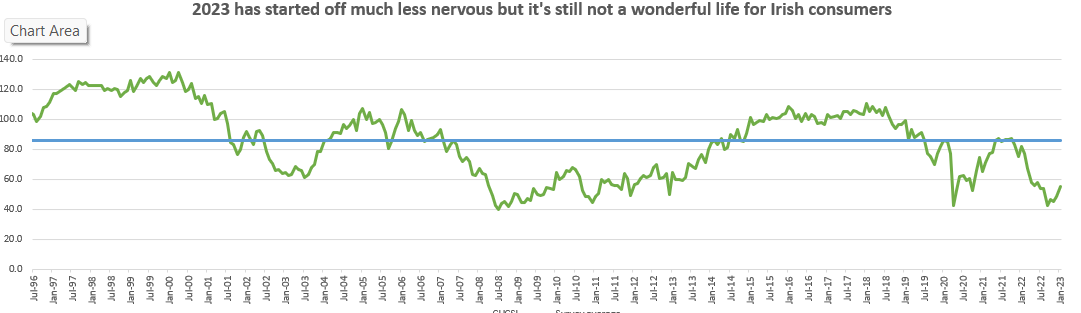

The Credit Union Consumer Sentiment Index, rose from 48.7 in December to 55.2 in January, putting the index at its strongest level since last June. The 6.5 point monthly increase was the largest since a 7 point gain in January 2022, a result that hints at some element of seasonal lift.

Our sense is that the switch over Christmas and new year away from the normal routine to less news-focussed time spent with family and friends may have eased consumer concerns somewhat. However, as the diagram below illustrates, at 55.2, the current consumer reading is some significant distance below the 85.6 point average of the now 27 years of Irish consumer sentiment survey data. This suggests Irish consumers remain very much aware of the economic and financial challenges that the new year holds.

All five main elements of the consumer sentiment survey showed improved readings in January relative to December, although the table above also shows how much weaker they are now than in January 2022. In contrast to the December results, the strongest month-on-month changes were in those elements of the survey focussed on household finances, rather than the broader economic climate.

This balance may suggest that many consumers feel they weathered the financial demands of Christmas better than feared while, perhaps, also benefitting from paying reduced attention to economic developments over the holiday period. Finally, the receipt of fiscal supports in the form of energy bill credits and 'Christmas bonus' welfare payments may also have assisted in the upgrade to the outlook for household finances.

The modest improvement seen in the January Credit Union Consumer Sentiment report in relation to consumer thinking about prospects for the Irish economy through the next twelve months was likely driven by very positive news on the 2022 outturn for the public finances, as well as continued low unemployment data during the survey period.

Consumer thinking regarding how their personal financial circumstances had evolved through the past twelve months was also modestly better in January than in December, possibly reflecting some easing in fuel costs but, at current levels, this element of the survey is still signalling major pressure on household finances.

Encouragingly, the improvement between December and January in consumer thinking in regard to household finances over the coming twelve months was more pronounced, perhaps suggesting that consumers think that the worst may behind them in terms of the pace of increase in the cost of living. Arguably, improved thinking in this regard could also owe something to expectations of significant and sustained fiscal support. In this context, it is notable that the Credit Union Consumer Sentiment Index has risen in three of the four months since Budget ’23 was delivered.

A sense that 2023 could prove difficult rather than disastrous for Irish consumers is also suggested by a marked pick-up in spending plans in the January sentiment reading. In part, this likely reflects bargain-hunting in the post-Christmas sales but even that implies that consumers are both able and willing to spend provided the offering is sufficiently attractive. This may be a tentative signal that many consumers sense that the worst could be over in terms of the intensity of price pressures facing their households.

Section II; What do Irish consumers think about their longer term economic and financial prospects?

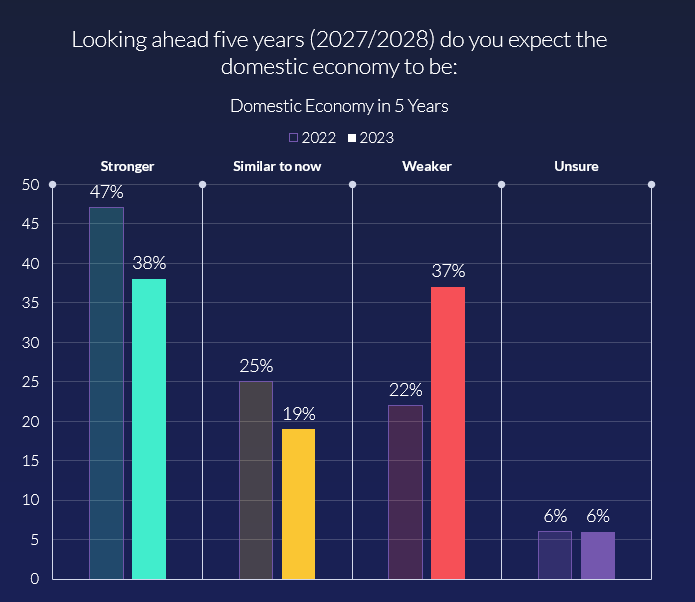

In recent years, a range of developments from the UK decision to leave the EU, through the pandemic and war in Ukraine have subjected Irish consumers to a sequence of large and disruptive shocks to their economic and financial circumstances. Understandably, these unpleasant surprises have framed consumer thinking on their short-term prospects, but have they also altered long-term thinking? As was the case in 2022, the January sentiment survey contained a number of special questions asking consumers how they expected a number of key economic metrics to develop on a five-year view.

The first question asked consumers about ‘macro’ growth prospects. As the diagram below illustrates, views are now broadly balanced as to whether economic growth will be stronger or weaker than in five years’ time. As the diagram also illustrates, this represents a markedly weaker assessment than that of a year ago.

The weakening in consumers’ views on the Irish economy’s longer-term prospects comes despite another markedly resilient performance in the past year in the face of extremely challenging global economic conditions. Our sense is that the downgrade may be due to a judgement that persistent pressures from an increasingly ‘stormy’ global environment are likely to take a toll on domestic growth prospects. A view that current cost-of-living pressures could continue or cause lasting strains may also have figured in consumer thinking of late. Increased nervousness about ‘tech sector prospects could also have contributed to a downgrade of the longer-term outlook. Finally, It might also be the case that consumers see domestic growth constraints in the shape of substantial bottlenecks in economic and social infrastructure and possibly skill shortages in some sectors as representing a major speedbump to the growth outlook.

As was the case a year ago, consumers outside Dublin, females and those on lower incomes were notably more negative on Irish economic prospects. However, in contrast to twelve months ago, younger consumers were notably downbeat, possibly reflecting particular concerns regarding to access to housing.

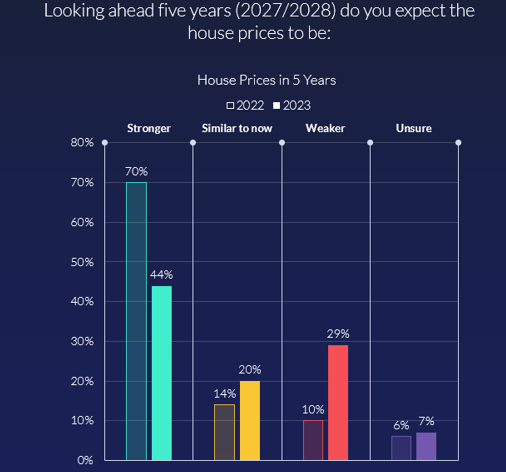

The January survey also asked consumers their views on the outlook for Irish house prices. Although the results shown in the diagram show a substantial downgrade from the 2022 survey, it remains the case that there is a clear balance of opinion that house prices will continue to increase materially. In this context, the proportion of consumers that envisage further increases is broadly unchanged.

There has been some increase in those expecting a correction in Irish house prices-from 10% a year ago to 29% now, presumably based on diminishing affordability and increased borrowing costs. The same factors mean there has been a sharp drop in those expecting persistent increases in property prices-from 70% a year ago to 44% in this survey.

As was the case in the previous survey, younger consumers tended to have a notably more negative view of the outlook for house prices than their older counterparts while females were also more negative than males but there were no pronounced geographic or income-related differences.

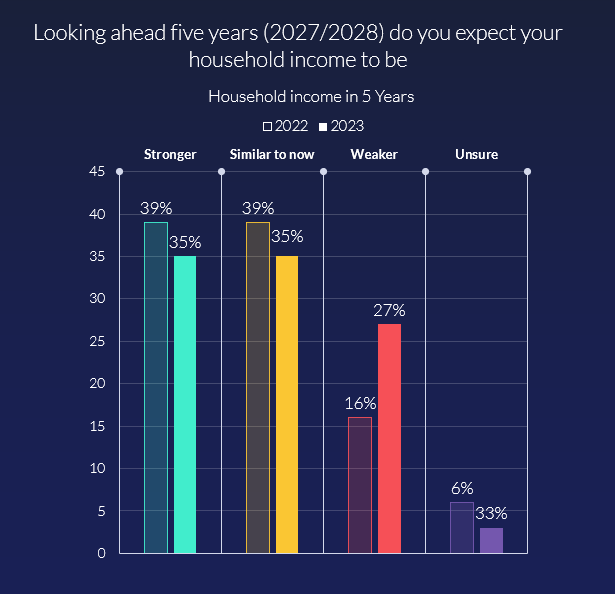

The January Credit Union Consumer Sentiment Survey, in partnership with Core Research, also asked consumers how they expected their household income to evolve through the next five years. The graph below shows responses to this question. The survey question didn’t specify if whether household income should be considered in nominal or inflation-adjusted terms. However, we would interpret the responses given as reflecting consumers views as to their purchasing power.

As the graph shows, there has been a marked weakening in Irish consumers’ expectations for their longer-term income prospects in the past twelve months. While there has been a clear drop in the share of consumers that expect their household income to be higher-from 39% to 35%, the more worrisome development is that a substantial 27% of consumers now think their household incomes will be weaker in five years’ time, markedly higher than the 16% who thought that a year ago.

The most negative responses to this question came from those who are currently struggling to make ends meet and from those aged 55 and older. The responses of the latter group may speak of concerns around inadequate pension provision that contrasts with the more positive expectation for house prices on the part of older consumers.

The Credit Union Irish Consumer Sentiment Survey is a monthly survey of a nationally representative sample of 1,000 adults. Since May 2019, Core Research have undertaken the survey administration and data collection for the Survey. The survey was live between the 4th-16th January 2023.

Section III; Introducing the Credit Union Consumer Sentiment Survey,in partnership with Core Research, for Northern Ireland.

Northern Ireland consumers remain nervous as 2023 begins

-

Negative sentiment dominates particularly in relation to the ‘macro’ environment

-

Northern Ireland economy seen weakening further in year ahead

-

Unemployment also seen climbing but to a lesser extent than softening in activity

-

Household finances under pressure, but 2023 not seen as widely negative as 2022

-

Consumers understandably cautious but not completely cancelling ‘big ticket’ spending

-

Special questions on five-year outlook suggest continuing economic strains but notably less negative consumer sentiment regarding personal finances and property prices.

This note sets out an analysis of the initial set of results for the Credit Union Consumer Sentiment survey for Northern Ireland. The survey fieldwork was undertaken by Core Research from January 4th to 17th.The survey methodology is the same as that of the Credit Union Consumer Sentiment Survey. The survey sample size is 350.

Not surprisingly, Northern Ireland consumers started 2023 in a nervous mood. On all key metrics, the Credit Union Consumer Sentiment Survey,shows negative responses significantly outnumbering positive responses. Yet, there are some modestly encouraging elements. Fewer consumers were negative in relation to the outlook for their household finances through the year ahead than was the case for the past twelve months and fewer again thought now was a bad time to make major household purchases.

On balance, the January reading for Northern Ireland was less downbeat than similar surveys for the UK as a whole but somewhat weaker than the comparable consumer sentiment reading for the Republic of Ireland. These comparative results appear consistent with materially different economic forecasts for the various areas as well as notably contrasting degrees of fiscal policy support at present.

The mood of the Northern Ireland consumer at the start of 2023

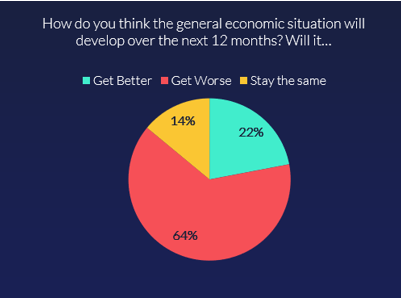

As the diagram below illustrates, two in three Northern Ireland consumers expect the general economic situation to weaken in the year ahead. Considering the overwhelmingly worrisome news flow around both global and local economic developments, this is not a surprising result. Arguably, a more notable finding is that just over one in five consumers sees scope for improvement in economic conditions in the next twelve months.

At the margin, those at both ends of the age spectrum tended towards more negative views as did those who reported difficulty making ends meet but overall, there was a broad consensus that 2023 is shaping up to be a difficult year for the Northern Ireland economy. Compared to similar surveys, Northern Ireland consumers appear to be notably less pessimistic than UK consumers as a whole but also somewhat more negative than their Republic of Ireland counterparts where negative views outnumbered positive by just over two to one. These results seem entirely consistent with the broad thrust of economic commentary and numerical forecasts for activity in the various areas.

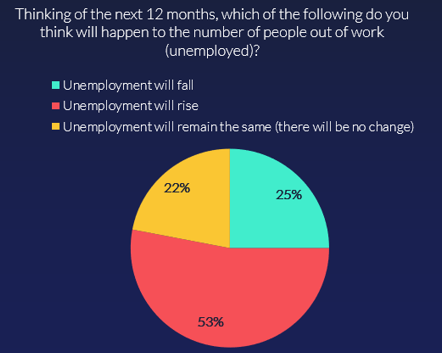

The Credit Union Consumer Sentiment survey,also asked Northern Ireland consumers how they felt unemployment would evolve over the next twelve months. The results illustrated in the diagram below show that the jobs market in Northern Ireland is expected to weaken. However, a comparison with expectations for economic activity might suggest that Northern Ireland consumers expect the jobs fallout to be relatively contained, perhaps hinting that they expect the degree of downturn may be limited.

Again, there was a generally negative view of the outlook for jobs across all demographics but notably more pessimistic responses were found among those at either end of the age spectrum (less than 25 years of age and over 55 years of age), among those with less education qualifications and among those currently struggling to make ends meet.

Consumer thinking in relation to the outlook for unemployment was broadly similar on both sides of the border but responses to the Republic of Ireland survey did not show the same age related variations that were evident in the Northern Ireland results.

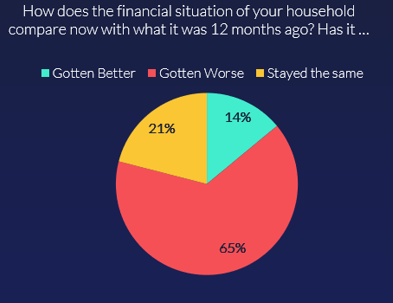

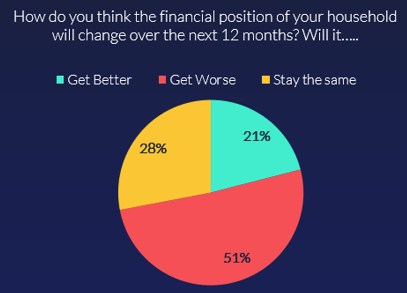

Northern Ireland consumers were also asked how their household finances now compared to those of twelve months ago. The responses, illustrated in the diagram below, appear to capture the widespread impact of cost-of-living pressures on consumers in Northern Ireland (and elsewhere).

Two out of every three consumers say their household financial circumstances have worsened in the past year. A small but not insignificant one in seven consumers report an improvement in their financial circumstances with these responses more common among younger and more highly educationally qualified consumers that likely reflects advances in employment and/or earnings on their part.

Northern Ireland consumers are understandably nervous about the prospects for their household finances through the year ahead. As the diagram below illustrates, roughly half of those surveyed expect their financial circumstances will worsen in the year ahead while just over one in four consumers expect an improvement in their household finances.

These results chime with the widespread expectation that while the rate of inflation may have peaked, it will remain elevated for some time to come, implying cost of living pressures will remain intense for many households. That said, the less negative balance overall in responses regarding household finances in the next twelve months compared to the past twelve months hints, at least tentatively, that some households feel they may now be past the worst. This improvement was more pronounced among younger consumers and those reporting a greater capacity to make ends meet at present.

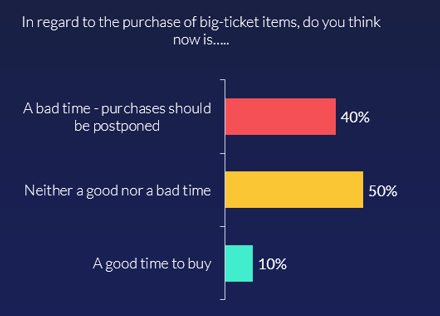

The final element of the Credit Union Consumer Sentiment Survey,for Northern Ireland attempts to assess the current buying climate by asking consumers if they think now is a good time to purchase ‘big ticket’ items such as furniture or large electrical goods. As the diagram below shows, Northern Ireland consumers are cautious in terms of making major financial outlays at present. This is to be expected in light of other elements of the survey.

Compared to similar surveys of UK consumers, the buying climate in Northern Ireland is modestly less negative, perhaps corresponding to the slightly less gloomy assessment of the general economic outlook. While the share of consumers who feel now is a good time to buy is not dissimilar in Northern Ireland and the Republic of Ireland, notably fewer consumers in the republic feel now current economic conditions make it a bad time to make large purchases.

What do Northern Ireland consumers think about their longer term economic and financial prospects?

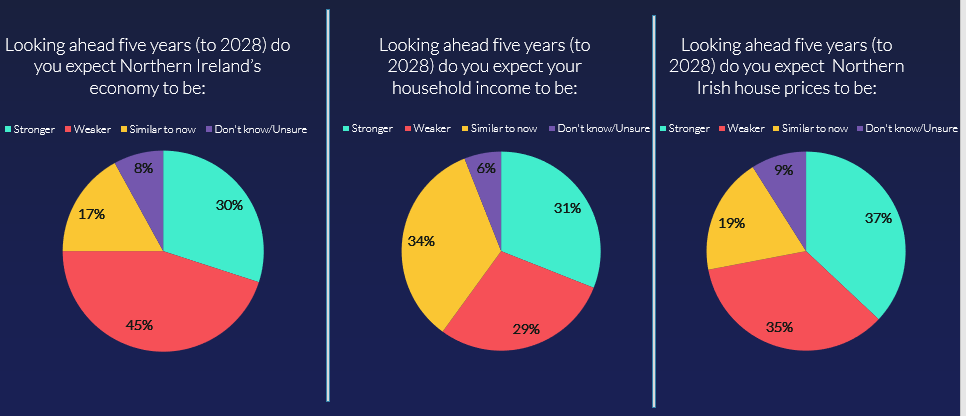

It is envisaged that each reading of the Credit Union Northern Ireland Consumer Sentiment Survey will contain an additional ‘special’ question dealing with a topical issue. While there is a very strong sense that economic and financial conditions facing Northern Ireland consumers will remain very challenging in the near term, a key unknown is whether present difficulties will prove temporary or persistent features of the environment facing Northern Ireland consumers. As a result, the January 2023 sentiment survey contained a special question asking how Northern Ireland consumers envisage the economic and financial landscape will look in five years’ time.

The responses given by Northern Ireland consumers to questions on the outlook for the general economy, their own household incomes and house prices are summarised in the diagram below.

As the diagram illustrates, negative sentiment continues to dominate in relation to the ‘macro’ outlook. However, concerns are less widespread than in relation to the twelve month outlook; the balance between negative and positive responses is much closer at -15 percentage points on a five year view than the -42 percentage point balance on a one year view. Encouragingly, views regarding the outlook for respondent’s own household finances move from a – 30 percentage point balance on a one-year view to a + 2 percentage point balance on a five-year view.

This result still suggests a significant three in ten Northern Ireland consumers expect a continued worsening in their living standards over the next five years, but it suggests sizeable numbers feel current pressures will begin to ease. In circumstances where- on balance-household incomes are seen increasing, it is not entirely surprising that house prices are also-on balance- seen increasing further.

Regarding the general economic outlook, Consumers are more positive in the Republic than in Northern Ireland. The difference between respective balances of + 1 percentage point and -15 percentage points is probably a reflection of the divergence in economic momentum in recent years. Viewed from the same perspective, the balance of responses in terms of the five-year outlook for household incomes at +7 percentage points in the Republic might be closer than expected to the +2 score for Northern Ireland. Finally, the wider 13-point gap between the expectations for house prices likely underscores the seemingly intractable imbalance between housing demand and supply in the republic.